House Mortgages And Also What You Should Find Out About Them

Written by-Pittman MahlerIf you're looking into home mortgages, then you surely are excited. It's time to buy a home! However, what you might realize is there is quite a lot of information to take in, and how do you sort all of this out to get to the mortgage company and product that you need? Keep reading to find out how to do this.

Know your credit score before beginning to shop for a home mortgage. If your credit score is low, it can negatively affect the interest rate offered. By understanding your credit score, you can help ensure that you get a fair interest rate. Most lenders require a credit score of at least 680 for approval.

Before getting https://www.businesswire.com/news/home/20211130005914/en/Changes-to-the-UBS-Group-Executive-Board , study your credit history. Good credit is what can help you get a mortgage. Obtain copies of your credit history and scores from the three major credit-reporting bureaus. Study your reports carefully to ensure that no issues or errors must be resolved before you apply. Many lenders need a minimum score of 680, which complies with Freddie Mac and Fannie Mae's guidelines. Most lenders want to avoid scores that are lower than 620.

Consider unexpected expenses when you decide on the monthly mortgage payment that you can afford. It is not always a good idea to borrow the maximum that the lender will allow if your payment will stretch your budget to the limit and unexpected bills would leave you unable to make your payment.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

Know how much you can afford to put towards your home mortgage. Do not rely on the lender to tell you the amount you qualify for, causing you to borrow the maximum amount. Try planning your budget and leaving some room for unexpected expenses. This is usually the case when you buy a home. You can use banking calculators to determine how much you can afford on a home and provide an estimate of the monthly mortgage payments.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

If you are having difficulty refinancing your home because you owe more than it is worth, don't give up. New programs (HARP) are in place to help homeowners out in this exact situation, no matter how imbalanced their mortgage and home value seems to be. Discuss a HARP refinance with your lender. If a lender will not work with you, go to another one.

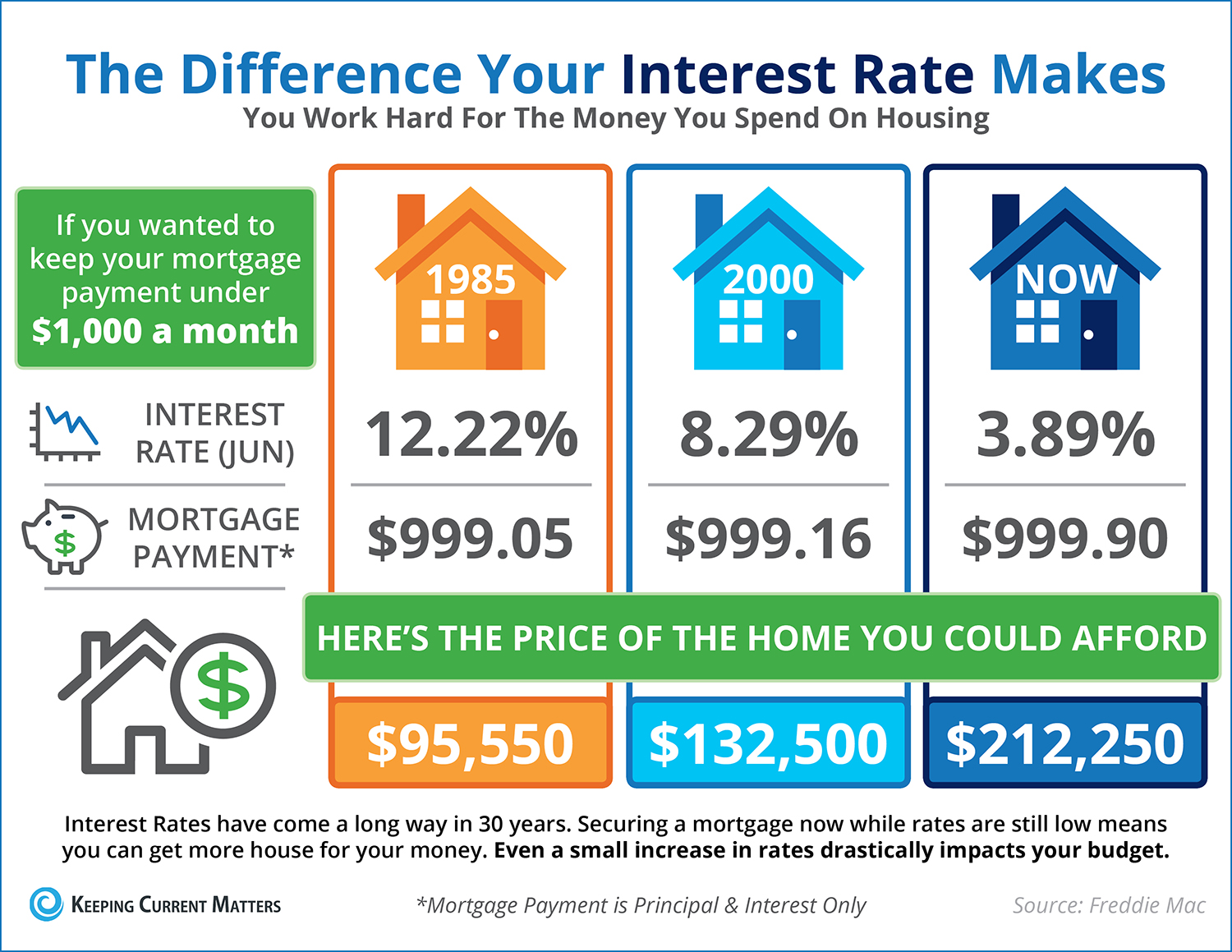

Be mindful of interest rates. How much you end up spending over the term of your mortgage depends on those rates. Of course, a higher interest rate means you pay more, but you should understand how even a one point difference can mean thousands of dollars over the life of the loan. If you aren't paying attention, you could pay more than you anticipated.

Don't apply for new credit and don't cancel existing credit cards in the six months before applying for a mortgage loan. Mortgage brokers are looking for consistency. Any time you apply for credit, it goes on your credit report. Avoid charging a large amount during that time and make every payment on time.

Consider a mortgage broker for financing. They may not be as simple as your local bank, but they usually have a larger range of available loans. Mortgage brokers often work with numerous lenders. This allows them to personalize your loan to you more readily than a bank or other finance provider.

Do not get confused with wording. Many people do not understand the difference between loans that are pre-approved or pre-qualified. When you are pre-approved a lender is potentially offering you the funds. When you are pre-qualified you are not being offered funds. Instead they are offering you a chance to become pre-approved.

If you have a little bit more money to put down on a home, consider getting a conventional mortgage as opposed to an FHA mortgage. FHA mortgages have lower down payments, but excessive fees that are added to the cost of the mortgage. Save up at least 5 percent in order to be eligible for an FHA loan.

You may want to consider refinancing your home mortgage. Interest rates have gone down a great deal in recent years, and due to this you could pay thousands less over the term of your loan if you refinance now. This is something that you must consider if you are pay just a fraction of a percent more than what you could pay now.

Be realistic when choosing a home. Just because your lender pre-approves you for a certain amount doesn't mean that's the amount you can afford. Look at your income and your budget realistically and choose a home with payments that are within your means. This will save you a lifetime of stress in the long run.

In a tight lending market, keeping your credit score high is key to getting a good mortgage rate. Obtain the credit scores from those three main agencies to be sure there aren't errors on it. To get the best possible loan rate these days, a score of at least 620 is probably needed.

Before signing on the dotted line of your home mortgage, learn about the history of the property you are purchasing. There are many things sellers and lenders are not required to disclose that you might find relevant. knowing whether or not your new home was the scene of a gruesome murder might be something you want to know before agreeing to buy.

When looking for a mortgage, compare the offers available from several brokers. A low interest rate is one major consideration. Also, you need to go over every type of loan that's out there. Also consider closing costs, down payment requirements and other associated fees.

When read the full info here asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

With the advice that has been given to you, you are now equipped to enter the mortgage market and begin deciding which route you want to take. It's important that you understand all of your options, and you want to feel in control and not thrown into a mortgage by a lender that doesn't fit your needs. Instead, go forth and get the right mortgage!